Posted:

RCL FOODS ANNUAL RESULTS MEDIA RELEASE 2018

PERFORMANCE HIGHLIGHTS

• 52,7% increase in headline earnings

• Exceptional performance from most grocery brands

• Strong Chicken recovery

• Sugar impacted by dumped imports

• Growth strategy gains momentum

Durban, 28 August 2018: RCL FOODS today reported a 52.7% increase in headline earnings for the year ended June 2018 despite a challenging trading environment. Profitability was boosted by a recovery in the Chicken business unit, strong growth through its brands and a focus on cost containment.

The company reported good progress in its “ONE RCL FOODS” transformation, a growth agenda which began four years ago and is focused on building a strong regional food business.

“Over the last four years we have built a more balanced and diversified portfolio. The next chapter of our agenda is to generate “sustainable quality of earnings” off the more stable base that we have created,” said CEO Miles Dally.

RCL FOODS said headline earnings growth was also driven by strong volume performances in the Dressings, Pet Food and Pies categories, lower interest costs and a tax credit related to an energy efficiency allowance in the Sugar business unit.

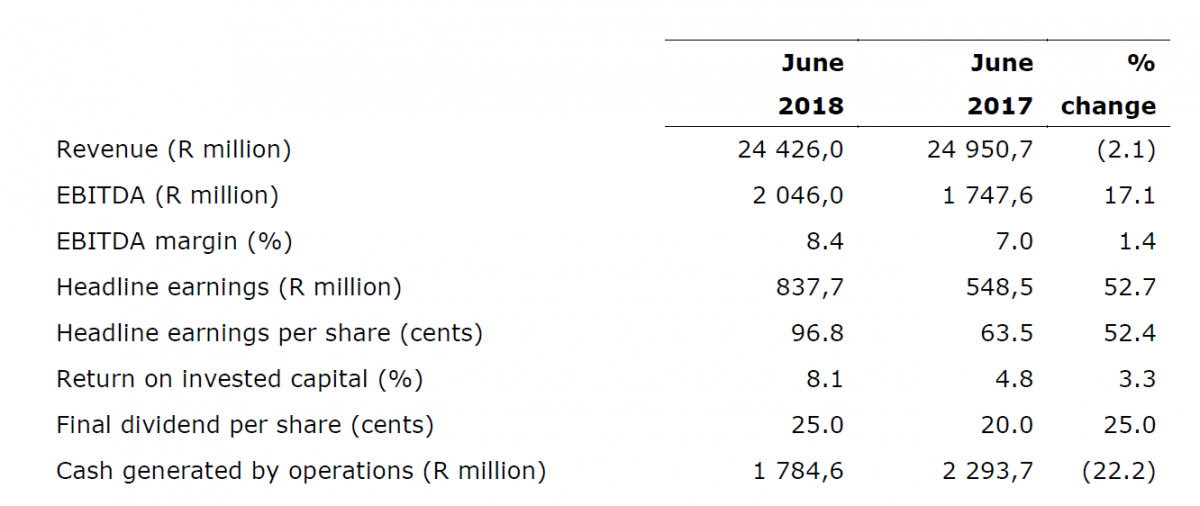

Headline earnings for the year ended June 2018 increased 52.7% to R837,7 million (2017: R548,5 million). Headline earnings per share was up 52.4% to 96.8 cents (2017: 63.5 cents).

Return on capital invested (ROIC) increased to 8.1% from 4.8% in 2017, largely driven by the improvement in underlying profitability. RCL FOODS measures its efficiency and effectiveness of capital application through ROIC.

Revenue and cash generation were both down. Revenue for the year totalled R24 426,0 million, a 2.1% decrease on the R24 950,7 million reported in 2017. The decrease was largely due to reduced volumes in the restructured Chicken business. Cash generated by operations was down 22.2% to 1 784,6 million (2017: 2 293,7 million.), largely due to a significant base effect of Chicken’s working capital release in the prior year.

RCL FOODS declared a final dividend of 25,0 cents per share (2017: 20,0 cents) bringing the total dividend for the year to 40,0 cents (2017: 30,0 cents).

Dally said he was pleased with the results, which had been achieved in a difficult year. “We have had to contend with the Listeriosis crisis and Avian Influenza (AI), both of which affected our chicken business as well as the significant impact of dumped imports on our chicken and sugar businesses.”

“These external challenges have forced us to think differently, find alternatives, drive efficiencies and reduce costs. The result has been a more resilient company, and a more profitable one.”

Cash on hand, net of overdrafts, has increased from R1 053,8 million in 2017 to R 1 263,4 million in 2018, mainly because of the improvement in underlying profitability.

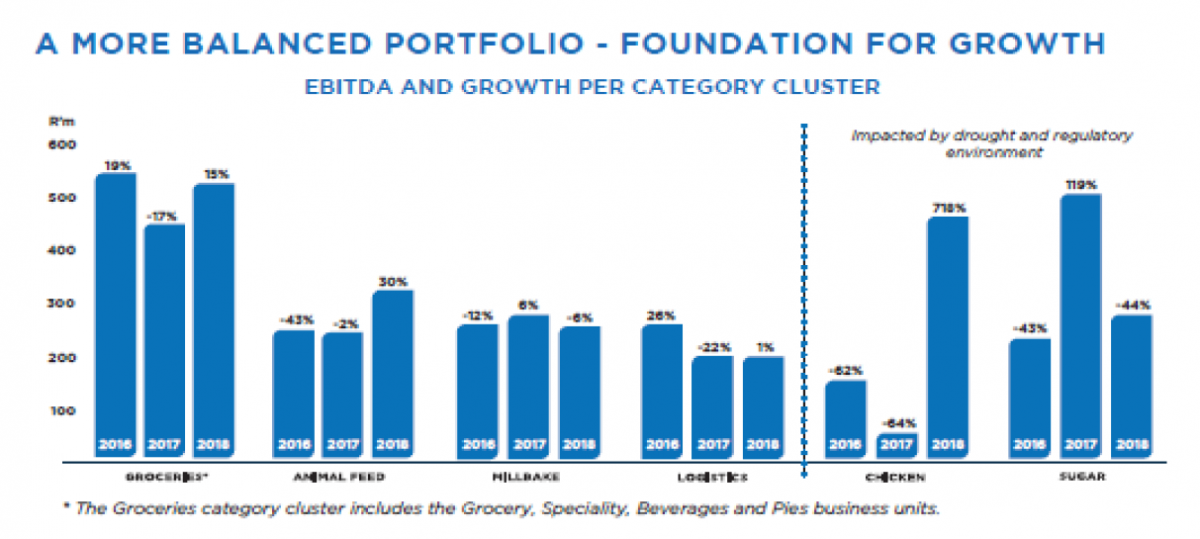

The major turnaround was in the Chicken business, which was forced to resize and restructure because of the impact of dumped chicken. The Chicken business unit EBITDA for the year improved 717.5% to R466,8 million at a margin of 6.7% (2017: R57,1 million at a margin of 0.7%.), despite the challenges of Listeria and AI.

The Chicken business restructuring has reduced production from 4.8 million birds to 3.4 million birds per week, resulting in a substantial proportion of low margin consequential (commodity) chicken being removed from the system.

The Chicken business recovery was the main reason that EBITDA in the Consumer division nearly doubled, rising 94.5% to R985,2 million (2017: R506,5 million). In the other two divisions, EBITDA in the Sugar and Milling division was down 16.1% to R869,0 million (2017: R1 036,1 million) while the Logistics division was up 0.6% to R204,3 million (2017: R203,1 million).

The Consumer division also benefitted from a significant improvement in the Groceries cluster. The strong branded groceries performance was a highlight of the year, given the deflationary environment, strong competition and no growth in the market.

The cluster reported market share gains, improved margins and an increase in the number of key brands which have become market leaders as a result of sound brand strategies and investment behind the brands.

The Sugar business was significantly impacted by dumped imports. The business reported a 6.3% increase in revenue, on the back of higher volumes after the drought, but EBITDA declined 44.0% to R284,1 million (2017: 507,0 million).

Increases in sugar production and improved efficiencies were more than offset by the impact of significant volume of dumped imports. The need to establish import parity to quell imports and excess supply drove significant local price decreases of more than 20% during the period. Furthermore, imports displaced local production volumes forcing a change in the sales channel mix towards higher exports at lower international prices leading to significant margin erosion.

“There is a strong focus within Sugar to ensure the continued sustainability of the business and the industry. In addition, alternative products and uses are being considered, with a simultaneous focus on improving productivity and efficiency to reduce costs further,” the company said.

Animal Feed, another business unit in the Sugar and Milling division, produced an acceptable result albeit supported by gains on maize and currency positions. EBITDA rose 30.2% to R319,5 million (2017: R245,4 million).

The merger of Molatek and Epol created one of South Africa’s largest animal feed businesses. RCL FOODS intends to grow more animal feed categories and expand into new markets and geographies.

Both Animal Feed and the Logistics division were affected by lower volumes from the restructured Chicken business.

Logistics division volumes were also affected by the listeriosis outbreak. Gains in new business and cost cutting resulted in a financial performance ahead of expectation and in line with the prior year. It generated revenue of R2,0 billion, marginally down on 2017.

A new long-term contract with Pick n Pay for their frozen category, including ice-cream, helped to offset the decline in chicken volumes.

The Millbake business unit generated an EBITDA of R265,4 million at a margin of 7.3% (2017: R283.7 million at a margin of 7.5%), down 6.5%. The business had a leadership change during the financial year and has set a recovery plan going forward.

The South African milling industry continues to be challenged by overcapacity and margins remain tight as a result. The focus remains on increasing volumes and improving efficiencies. Baking’s results were disappointing. Operational challenges including prolonged strike action as well as competitor pressure impacted volumes and margins.

RCL FOODS estimated the financial impact of the listeriosis crisis at R158,2 million – once-off costs of R78,2 million for product recall and the restoration of the Rainbow brand, and an estimated R80,0 million as lost contribution.

The outbreak, which resulted in more than 180 deaths earlier in 2018, was and remains a major crisis for the local food industry and the country. The company has implemented number of additional safety measures at production facilities, over and above the international food safety standards already followed.

“Given that we have never had listeria in our products at our Wolwehoek plant, and have subsequently been cleared of the ST6 ‘outbreak strain’ of listeria, we have been working to restore consumer trust both in our Rainbow brand and the chilled processed meats category,” the company said.

RCL FOODS is continuing its cautious expansion into Africa. It has a low-risk expansion strategy, cautious of economic and political risk. The focus has been narrowed to mainly SADC countries, and whilst acquisitions have been evaluated, none have so far been effected. The company is finalising a 45% shareholding in an FMCG distribution operation based in Lusaka, Zambia which will provide a re-entry into the Zambian market.

Looking forward, RCL FOODS expected the recent modest recovery in market volumes to continue. “Trading conditions will continue to be challenging and the fight for market share will remain fierce,” it said.